4.1 Measuring Market Attractiveness

Four key factors in selecting global markets are:

- market’s size and growth rate

- particular country or region’s institutional contexts

- region’s competitive environment

- market’s cultural, administrative, geographic, and economic distance from other markets the company serves.

Market Size and Growth Rate

There is no shortage of country information for making market portfolio decisions. A wealth of country-level economic and demographic data are available from a variety of sources including governments, multinational organizations such as the United Nations or the World Bank, and consulting firms specializing in economic intelligence or risk assessment. However, while valuable from an overall investment perspective, such data often reveal little about the prospects for selling products or services in foreign markets to local partners and end users or about the challenges associated with overcoming other elements of distance. Yet many companies still use this information as their primary guide to market assessment simply because country market statistics are readily available, whereas real product market information is often difficult and costly to obtain.

What is more, a country or regional approach to market selection may not always be the best. Even though Theodore Levitt’s vision of a global market for uniform products and services has not come to pass, and global strategies exclusively focused on the “economics of simplicity” and the selling of standardized products all over the world rarely pay off, research increasingly supports an alternative “global segmentation” approach to the issue of market selection, especially for branded products. In particular, surveys show that a growing number of consumers, especially in emerging markets, base their consumption decisions on attributes beyond direct product benefits, such as their perception of the global brands behind the offerings.

Specifically, research by John Quelch (2003) and others suggests that consumers increasingly evaluate global brands in “cultural” terms and factor three global brand attributes into their purchase decisions: (a) what a global brand signals about quality, (b) what a brand symbolizes in terms of cultural ideals, and (c) what a brand signals about a company’s commitment to corporate social responsibility. This creates opportunities for global companies with the right values and the savvy to exploit them to define and develop target markets across geographical boundaries and create strategies for “global segments” of consumers. Specifically, consumers who perceive global brands in the same way appear to fall into one of four groups:

- Global citizens rely on the global success of a company as a signal of quality and innovation. At the same time, they worry whether a company behaves responsibly on issues like consumer health, the environment, and worker rights.

- Global dreamers are less discerning about, but more ardent in their admiration of, transnational companies. They view global brands as quality products and readily buy into the myths they portray. They also are less concerned with companies’ social responsibilities than global citizens.

- Antiglobals are skeptical that global companies deliver higher-quality goods. They particularly dislike brands that preach American values and often do not trust global companies to behave responsibly. Given a choice, they prefer to avoid doing business with global firms.

- Global agnostics do not base purchase decisions on a brand’s global attributes. Instead, they judge a global product by the same criteria they use for local brands (Holt et al., 2004).

Companies that use a “global segment” approach to market selection, such as Coca-Cola, Sony, or Microsoft, to name a few, therefore must manage two dimensions for their brands. They must strive for superiority on basics like the brand’s price, performance, features, and imagery, and, at the same time, they must learn to manage brands’ global characteristics, which often separate winners from losers. A good example is provided by Samsung, the South Korean electronics maker. In the late 1990s, Samsung launched a global advertising campaign that showed the South Korean giant excelling, time after time, in engineering, design, and aesthetics. By doing so, Samsung convinced consumers that it successfully competed directly with technology leaders across the world, such as Nokia and Sony. As a result, Samsung was able to change the perception that it was a down-market brand, and it became known as a global provider of leading-edge technologies. This brand strategy, in turn, allowed Samsung to use a global segmentation approach to making market selection and entry decisions.

Institutional Contexts

Khanna and others (2005) developed a five-dimensional framework to map a particular country or region’s institutional contexts. Specifically, they suggest careful analysis of a country’s:

- political and social systems,

- openness,

- product markets,

- labour markets, and

- capital markets.

Political System

A country’s political system affects its product, labour, and capital markets. In socialist societies like China, for instance, workers cannot form independent trade unions in the labour market, which affects wage levels. A country’s social environment is also important. In South Africa, for example, the government’s support for the transfer of assets to the historically disenfranchised native African community has affected the development of the capital market.

Openness

The more open a country’s economy, the more likely it is that global intermediaries can freely operate there, which helps multinationals function more effectively. From a strategic perspective, however, openness can be a double-edged sword: a government that allows local companies to access the global capital market neutralizes one of the key advantages of foreign companies.

Product markets

Even though developing countries have opened up their markets and grown rapidly during the past decade, multinational companies struggle to get reliable information about consumers. Market research and advertising are often less sophisticated and, because there are no well-developed consumer courts and advocacy groups in these countries, people can feel they are at the mercy of big companies.

Labour Markets

Recruiting local managers and other skilled workers in developing countries can be difficult. The quality of local credentials can be hard to verify, there are relatively few search firms and recruiting agencies, and the high-quality firms that do exist focus on top-level searches, so companies scramble to identify middle-level managers, engineers, or floor supervisors.

Capital Markets

Capital and financial markets in developing countries often lack sophistication. Reliable intermediaries like credit-rating agencies, investment analysts, merchant bankers, or venture capital firms may not exist, and multinationals cannot count on raising debt or equity capital locally to finance their operations.

Emerging economies present unique challenges. Capital markets are often relatively inefficient and dependable sources of information, scarce while the cost of capital is high and venture capital is virtually nonexistent. Because of a lack of high-quality educational institutions, labour markets may lack well-trained people requiring companies to fill the void. Because of an underdeveloped communications infrastructure, building a brand name can be difficult just when good brands are highly valued because of lower product quality of the alternatives. Finally, nurturing strong relationships with government officials often is necessary to succeed. Even then, contracts may not be well enforced by the legal system.

Competitive Environment

The number, size, and quality of competitive firms in a particular target market compose a second set of factors that affect a company’s ability to successfully enter and compete profitably. While country-level economic and demographic data are widely available for most regions of the world, competitive data are much harder to come by, especially when the principal players are subsidiaries of multinational corporations. As a consequence, competitive analysis in foreign countries, especially in emerging markets, is difficult and costly to perform and its findings do not always provide the level of insight needed to make good decisions. Nevertheless, a comprehensive competitive analysis provides a useful framework for developing strategies for growth and for analyzing current and future primary competitors and their strengths and weaknesses.

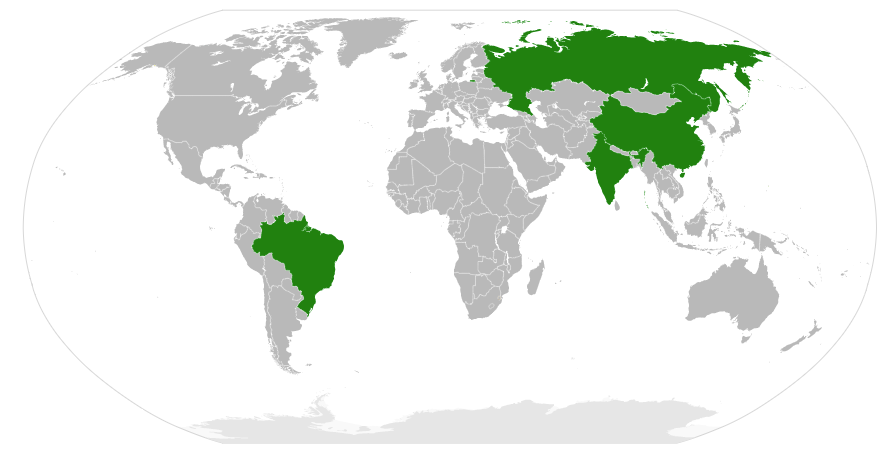

Case: Which BRIC Countries? A Key Challenge for Carmakers

Today, automobile manufacturers face a critical challenge: deciding which BRIC countries (Brazil, Russia, India, and China) to bet on. In each, as per capita income rises, so will per capita car ownership—not in a straight line but in classic “S-curve” fashion. Rates of vehicle ownership stay low during the first phases of economic growth, but as the GDP or purchasing power of a country reaches a level of sustained broad prosperity, and as urbanization reshapes the work patterns of a country, vehicle sales take off. But that is about where the similarities end. Each of the four BRIC nations has a completely different set of market and industry dynamics that make decision choices about which countries to target, including making difficult decisions about which markets to avoid, extremely difficult.

For one thing, vehicle manufacturing is a high-profile industry that generates enormous revenue, employs millions of people, and is often a proxy for a nation’s manufacturing prowess and economic influence. Governments are extensively involved in regulating or influencing virtually every aspect of the product and the way the industry operates—including setting emissions and safety standards, licensing distributors, and setting tariffs and rules about how much manufacturing must take place locally. This reality makes the job of understanding each market and appreciating the differences more vital. For example, a summary overview of the BRIC nations reveals the differences among these markets and the operating complexities in all of them.

Brazil, with Russia, is one of the smaller BRIC countries, with 188 million people (by comparison, China and India each have more than 1 billion, Russia has 142 million). Yet car usage is already relatively high: 104 cars in use per 1,000 people, nearly 10 times the rate of usage in India, according to the Economist Intelligence Unit. Because of this, growth projections for Brazil are relatively low—more in line with developed nations than with the other BRIC countries. Projections made by the industry research firm Global Insight show that sales will grow just 2% until 2013, underperforming even the U.S. market’s projected growth rate.

On the plus side, Brazil is socioeconomically stable, with increasing wealth and a maturing finance system that is helping to propel growth among rural, first-time buyers who prefer compact cars. Few domestic brands exist, as the market is dominated by GM, Ford, Fiat, and Volkswagen. Prompted by generous government incentives, high import taxes, and exchange rate risks, foreign automakers have invested significantly in Brazil, which has thus become an unrivaled production hub for the rest of South America. Brazilian consumers live in a country with large rural areas and very rough terrain; they demand fairly large, SUV-like cars, made with economical small engines and flex-fuel power trains friendly to the country’s biofuel industry. When a Latin American family buys its first automobile, chances are it was made in Brazil.

Given Russia’s proximity to Europe, consumer preferences there are more akin to those of the developed markets than to those of China or India, and expensive, status-enhancing European models remain popular, although European safety features, interior components, and electronics are often stripped out to reduce costs. For vehicle manufacturers, the attractions of the Russian market include an absence of both local partnership requirements and significant local competitors. But there is high political risk. So far, the Russian government has permitted foreign carmakers to operate relatively freely, but the Kremlin’s history of meddling in private enterprise and undercutting private ownership worries some executives. These concerns were heightened in November 2008, when Russia implemented tariffs against car imports in hopes of avoiding layoffs that might spark labour unrest among the country’s 1.5 million car industry workers.

India has 1.1 billion people, but its level of car adoption is still low, with only 11 cars in use per 1,000 people. The upside is higher potential growth: among the BRIC countries, India is expected to have the fastest-growing auto sales, almost 15% per year until 2013, according to Global Insight. Sales of subcompact cars are strong, even during the global recession. The popularity of these small cars combines with India’s energy shortages and the country’s chronic pollution to provide foreign carmakers with an ideal opportunity to further develop electric power-train technologies there.

Until the early 1990s, foreign automobile manufacturers were mostly shut out of India. That has changed radically. Today, foreign automakers are welcomed and the government promotes foreign ownership and local manufacturing with tax breaks and strong intellectual property protection. And because foreign companies were shut out for a long period of time, India has capable manufacturers and suppliers for foreign vehicle manufacturers to partner with. Local competition is strong but is thus far concentrated among three players: Maruti Suzuki India, Ltd., Tata, and the Hyundai Corporation, which is well established in India.

China is almost as large as the other three combined in total auto sales and production. Its overall auto usage is just 18 cars per 1,000 households, but annual sales growth until 2013 is expected to be almost 10%. Its size and growth potential make China a dominant force in the industry going forward; new models and technologies developed there will almost certainly become available elsewhere.

But the Chinese government plays a central role in shaping the auto industry. Current ownership policies mandate that foreign vehicle manufacturers enter into 50-50 joint ventures with local automakers, and poor intellectual property rights enforcement puts the design and engineering innovations of foreign car companies at constant risk. At the same time, to cope with energy shortages and rampant pollution, the Chinese government is strongly encouraging research and development on alternative power trains, including electric cars and gasoline-electric hybrids. As a result, Chinese car companies may develop significant power-train capabilities ahead of their competitors.

Like their Indian counterparts, Chinese car companies have outpaced global automakers in developing cars specifically for emerging markets. A few Western companies, like Volkswagen AG, which has sold its Santana models in China through a joint venture (Shanghai Volkswagen Automotive Company) since 1985, are competitive. Some Chinese carmakers, like BYD Company, aspire to become global leaders in the industry. But many suffer from a talent shortage and inexperience in managing across borders. This may prompt them to acquire all or part of distressed Western automobile companies in the near future or to hire skilled auto executives from established companies and their suppliers.

In short, each of the four BRIC nations has a completely different set of market and industry dynamics. And the same is true for the other developing nations. Meanwhile, the number of autos in use in the developing world is projected to expand almost six-fold by 2018.

(Haddock & Jullens, 2009)

Cultural, Administrative, Geographic, and Economic Distance

Explicitly considering the four dimensions of distance can dramatically change a company’s assessment of the relative attractiveness of foreign markets. In his book, The Mirage of Global Markets, David Arnold describes the experience of Mary Kay Cosmetics (MKC) in entering Asian markets. MKC is a direct marketing company that distributes its products through independent “beauty consultants” who buy and resell cosmetics and toiletries to contacts either individually or at social gatherings. When considering market expansion in Asia, the company had to choose: enter Japan or China first? Country-level data showed Japan to be the most attractive option by far: it had the highest per capita level of spending on cosmetics and toiletries of any country in the world, disposable income was high, it already had a thriving direct marketing industry, and it had a high proportion of women who did not participate in the work force. MKC learned, however, after participating in both markets, that the market opportunity in China was far greater, mainly because of economic and cultural distance: Chinese women were far more motivated than their Japanese counterparts to boost their income by becoming beauty consultants. Thus, the entrepreneurial opportunity represented by what MKC describes as “the career” (i.e., becoming a beauty consultant) was a far better predictor of the true sales potential than high-level data on incomes and expenditures. As a result of this experience, MKC now employs an additional business-specific indicator of market potential within its market assessment framework: the average wage for a female secretary in a country (Arnold, 2004, p. 34).

MKC’s experience underscores the importance of analyzing distance. It also highlights the fact that different product markets have different success factors: some are brand-sensitive while pricing or intensive distribution are key to success in others. Country-level economic or demographic data do not provide much help in analyzing such issues; only locally gathered marketing intelligence can provide true indications of a market’s potential size and growth rate and its key success factors.

Core Principles of International Marketing – Chapter 6.1 by Babu John Mariadoss is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License, except where otherwise noted.

{kind=link}