Welcome to the economic study of us – the human population. How does the way we are born, grow, age, and die affect the economy, and how does the economy affect the way we are born, grow, age, and die?

These questions take a limited view of us as human beings. The approach is materialistic. To move forward without acknowledging the limitations of this view would be dangerous. Next thing you know, we would be pricing human life in dollars without batting an eye. We do actually discuss the dollar value of a decreased chance of dying, known as the “Value of a Statistical Life”, in Chapter 10.

We can move forward with economics and demography if we understand that economics cannot provide ultimate, absolute, or intrinsic values for anything. Economics just measures the material trade-offs involved in decisions or policies. In economics, the value of something is what must be given up in exchange for one more unit of it. To be specific, economics measures the value-in-trade of the marginal unit of a good or service to market participants at one point in time.

The value-in-trade does not tell us what to buy or do; it tells us what it will cost to do so. It tells us what we have to give up to get what we want. Economic demography provides us with some of the information we need to support those social outcomes we believe are best.

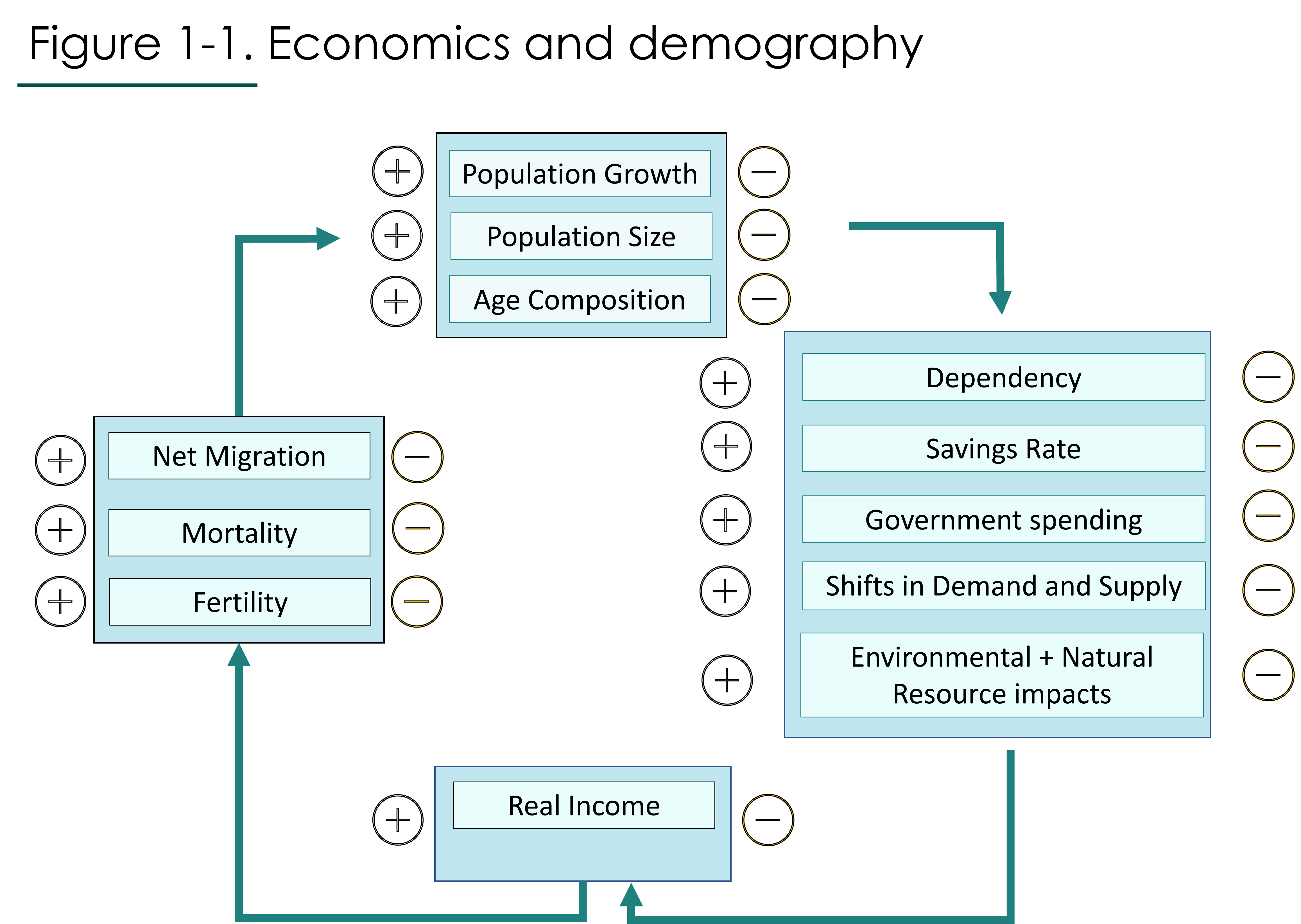

Figure 1.1 shows that the economy and the population’s size, growth rate, and composition are mutually influential, as explained by J.R. Weeks (1989). Financial pressures, especially those that increase (+) or decrease (-) real income[1], may lead to increases or decreases in fertility, mortality, and migration. This is shown by the lower left arrow.

Fertility, mortality, and migration are the three drivers of population change. When they change, the population’s growth rate, absolute size, and age or sex composition may change. This is shown by the upper left arrow.

Changes in the population’s growth rate, absolute size, and age or sex composition affect the economy, for example by changing the supply of labour and the demand for resources. Prices and wages change, and real income is affected. Thus, as shown by the top right and lower right arrows, changes in the overall population increase or decrease real income. We come full circle.

Since economics and demography affect one another, there is the possibility of feedback loops. The population’s growth could cause the economy to grow, which could cause the population to grow, and so on forever and ever without rest.

On the other hand, the causality between population and the economy could be such that an equilibrium emerges. An equilibrium is a resting place, a stable situation from which there is no tendency to move. If a randomly occurring phenomenon from outside economics or demography, that is to say, some phenomenon exogenous to the model, were to upset an equilibrium, the equilibrium would eventually re-emerge.

In our next chapter we’ll examine the equilibrium described by the oldest model of population and economic change, the Malthusian model.

1. The cost of a loaf of bread is $3.99. The average wage is $12 per hour. What does this mean to an economist?

2. What determines value-in-trade?

3. Compare the benefits of the legal system to society with the benefits of the market-place to society.

4. What is an equilibrium?

5. Give an example of a positive feedback loop that involves war.

6. Give an example of a negative feedback loop that involves sleep.

- Real income equals income divided by the price index, thus real income is a measure of purchasing power. ↵

Real income is income divided by a price index. The price index measures the cost of living. Thus, your real income measures how much stuff you can buy with your income.

Fertility refers to how many biological children people have. See Age-specific fertility rate, Completed fertility rate, General fertility rate, and Total fertility rate for some precise definitions.

Mortality refers to death. See Age-specific mortality, Crude death rate, Expected life years remaining, and Standardized death rate for more specific definitions.

Migration refers to the movement of people from one place to another. See Emigration, Immigration, and Net Migration for more specific definitions.