15 Balanced Scorecard

Strategic Management: Balanced Scorecard

“What you measure is what you get”

(Kaplan and Norton, 1992: 71)

Introduction

The balanced scorecard (BSC) is a strategic management and planning tool used by many organizations. It focuses on aligning daily work with the organization’s strategy while putting in place specific measures that allow management to progress towards strategic targets.

The BSC concept was first suggested by Kaplan and Norton in 1992 to evaluate financial and non-financial performance measurements. They were able to conceive the idea after examining the top corporations in the world and how they were run. The scorecard provides managers with a comprehensive framework to assess both tangible and intangible assets in the corporation (Kaplan and Norton, 2001a). While focusing on four perspectives (financial goals, customer satisfaction, internal processes, and learning and growth), companies are able to effectively evaluate their overall performance.

The BSC helps individual organizations evaluate their performance based on their own strategy and internal environment. It can set the stage for developing performance measures on the basis of two specific characteristics: transparency and strategy orientation.

What makes the BSC effective is its capability to convert the organization’s strategy to practical measures (Kaplan and Norton, 2001a). The BSC also suggests that intangible assets play a significant role in creating an organization’s value (Nolan Norton Institute, 1991). Intangible assets are objects the company owns that are not physically available. This includes intellectual property (i.e. patents and trademark), human capital (i.e. employees’ talent) and customer loyalty (Kaplan and Norton, 2009). On the other hand, tangible assets are of the physical form and include machinery, buildings, and lands.

According to Norton and Kaplan, in order to improve the management of their intangible assets, corporations are required to incorporate the non-financial measures to their management systems. It should be noted that intangible assets rarely make value by themselves, instead they should be integrated into other intangible and tangible assets to generate value. For example, with the implementation of a new growth-oriented sales strategy in the organization, different aspects should be aligned. This includes knowledge about customers, databases, organization structure, and incentive compensation program.

Management systems contain many interrelated parts which need concurrent coordination among different line and staff units in the corporation. Independent functions such as budgeting, human resources, and process management should be coordinated to make the strategic alignment. Indeed, they should act as an integrated system rather than a set of independent sub-systems. To align different units and personnel to the strategy, the BSC suggests three efficient tools: strategy map, dashboard, and scorecards.

Strategy Map:

The concept of the strategy map, (Kaplan & Norton 2000, 2001, 2004), illustrates causal relationships between project objectives. For instance, training personnel can boost service quality which in turn leads to higher customer satisfaction, increased customer loyalty and eventually higher revenues and margins.

All the objectives are connected to each other through cause and effect relationships. These interactions begin from employees, pass through processes and customers, and end with financial outcomes.

Retrieved from: https://www.balancedscorecard.org/BSC-Basics/About-the-Balanced-Scorecard

Dashboard:

The dashboard is a set of measures that provide managers with information regarding various operations and processes within the organization. It demonstrates current progress on an operational level and therefore allows managers to get an idea of the current state of the company.

Retrieved from: https://bscdesigner.com/dashboard-vs-balanced-scorecard.htm

Scorecards:

While the dashboard is used as a way of measuring performance, the scorecard is used to manage performance. Scorecards use key performance indicators (KPIs; critical indicators of progress toward an intended result) as a tool to measure progress in order to plan and execute the company’s strategy. Kaplan and Norton compare scorecards to an “airplane cockpit providing the pilot with detailed information about several aspects of the flight” (Kaplan and Norton, 1992) which ultimately allow future planning.

Retrieved from: https://bscdesigner.com/dashboard-vs-balanced-scorecard.htm

The four perspectives

As mentioned earlier, in order to be well-rounded and successful, the BSC suggests that the company views itself from four perspectives and consequently develop objectives, measures (KPIs), targets and initiatives that are in relation to these points of view. Generally speaking, companies can follow the proposed hierarchy of perspectives (from top to bottom: Financial → Customer → internal processes → learning and growth), yet it’s important to note that it is encouraged to tailor the BSC to the company’s strategy and needs, consequently arranging the perspectives as required.

- Financial perspective:

When an organization begins creating a BSC, how they will want to improve financially will come as an initial concern. For example, the financial perspective for start-ups is about survival as they need the cash flow to help them stay afloat. However for more established companies, their financial perspective should look to keep their shareholders happy and keep them invested in their company.

This is where a business will develop their goal as it will give an organization more specificity with their project. For example, tech companies may look for revenue growth on a new product. Accounting, consulting and law firms may focus on increasing profit margins. A company is then able to track their goals with key performance indicators (KPI’s). KPI’s are measurements that are linked to the goal that is the best way to follow the success of a project. These can include cash flow, total asset holding, market price per share, total expenses and revenue per employee. More can be seen from this website here https://bscdesigner.com/sample-kpis.htm.

The financial objective is also a consequence of the other three objectives so they will have to be connected and balanced. Even though a lot of companies are aimed at being financially successful, the top companies in the world have shown that a balance of all four perspectives is their key to success (De Wet, Johannes & Jager, Phillip, 2007).

- Customer perspective:

The Customer perspective addresses how a company creates value for its customers (Atkinson et al. 2012). For this perspective, the objectives are to fulfill their consumers’ value propositions and to create win-win partnerships in order to strengthen dealer and distributor relationships. If the organization is able to meet these objectives, it should see a positive effect on its financials because happy consumers continue to buy from organizations that treat them well. If the organization is unable to meet these objectives, their financials will suffer.

However, the outcome of the Customer perspective, “Delight the consumer” is not explicitly linked to the Financial perspective. It is a general belief that if consumers are delighted, they should buy more products. The first step in developing this perspective is to define its customer/market segments (Figge, Hahn, Schaltegger and Wagner 2002). Once a company has identified its market segment, it was suggested that the company selects two sets of measures: generic measures (market share, customer retention, customer acquisition, customer satisfaction, and customer profitability) and performance drivers (product/service attributes, customer relationship, and company image and reputation) (Kaplan and Norton 1996a). Second, the company must determine what customers value and define how they differentiate (performance drivers) themselves from other companies to retain, attract, and satisfy (generic measures) their target customers (Kaplan and Norton 2001). In sum, the Customer perspective uses a value proposition to describe the product, price, and image that a company offers.

- Internal processes perspective:

This perspective focuses on the objectives necessary to satisfy both customer and financial needs. That being, the company must develop “internal processes” which are the core/critical business processes where the company creates value (Kaplan and Norton, 2001). To do so, a corporation can either improve existing business systems or develop new business systems.

This perspective is best understood when presented with examples. For instance, when a company’s mission is to be a leader in product development, established objectives revolve around the creation and development of products. Therefore, in relation to the customer perspective, the internal perspective could in return develop products that satisfy those needs. Looking at Apple, it has developed its camera in order to satisfy the customer’s need to capture moments with their phone. On the other hand, when a company focuses on operational excellence, the internal perspective will aim to satisfy objectives such as decreasing running costs, increasing product quality or optimizing the supply chain.

Similar to the rest, this perspective is interdependent with all other perspectives. Although it serves a specific subgroup of the balanced scorecard, it ultimately serves the overarching mission of the company. Another important thing to note when developing the internal perspective is to not use binary indicators when assigning KPI’s to the objectives. Binary indicators are those that have two possible values/states (i.e. complete/incomplete). The issue with such indicators is that they don’t grant us control over the progress of the company. The team’s knowledge is limited to whether the objective is completed or not, and therefore nothing is known about how far along we are from completion. Moreover, having a binary indicator could reduce the team’s ambition since there is no set target that will push the team’s performance (instead of hitting a quantified target, the team only aims to complete the task). In order to avoid binary indicators, objectives must be correctly formulated/worded.

- Learning and growth perspective:

“Learning and Growth” is the extent to which a company should learn and develop its vision. According to Kaplan and Norton, ‘learning’ is more important than ‘training’ which contains mentoring and coaching in the corporation. This perspective also evaluates the flow of information among employees. That is how easy the communication between workers is that let them resolve the problems efficiently.

Furthermore, this perspective determines the extent to which a company must learn in order to fulfill the customer’s expectations, improve internal processes, and obtain financial objectives.

Through the measurement of “Learning and Growth” perspective managers can develop the following capabilities:

- Employee capabilities: Managers can provide employees with the necessary skills aligned with the strategy. Moreover, they give personnel the opportunity to obtain a better understanding of different functions of the company such as marketing, sales, etc.

- Information system capabilities: They can figure out what information systems such as CRM, ERP, BMP that organization may require to implement the strategy effectively.

- Strategy awareness and motivation: Managers can motivate and align employees by holding specific programs about the understanding and implementation of the strategy.

learning and growth constitute the essential foundation for the success of any knowledge-worker organization. In a knowledge-worker organization that the employees are the core resource and due to the rapid technological change, it is vital for the organization to provide workers with continuous learning. BSCs help managers focus on learning programs where they can have the biggest contribution in the execution of strategy.

BSC’s advantages:

Kaplan and Norton (1996a), suggest several benefits to applying the BSC in companies:

- Clarify and reach consensus about strategy.

- Communicate strategy across the company.

- Align sectors and employees’ goals to the strategy.

- Make a connection between strategic objectives and long-term goals and annual budgets.

- Determine strategic initiatives.

- Conduct periodic evaluation and systematic reviews based on strategy.

- Receive feedback for improving strategy.

BSC’s disadvantages:

Disadvantages of having a focus: Excessive focus on one strategy could ruin the business. Although It is important to have a specific focus on a trademark area of expertise for the company, there is a need to take care of other aspects of the company and keep a “balanced” focus.

How to implement a Balanced Scorecard.

- Establish company strategy/vision/mission.

This is what will determine the direction of the company and build the framework for the perspectives that will be put in place. Although they are superficial and can be tailored to best suit the company, there are 3 generic strategies that a company can adopt (Kaplan and Norton, 2001):

-

-

- Product Leadership Strategy (creating new products and services; build the franchise).If it is heavily reliant on tech, the company can focus on this strategy. The objectives are mainly focused on:

- Developing new products.

- Innovating existing products.

- Improving speed to market.

- Customer Intimacy Strategy (improving existing products or customer service; increase customer value).Here, the company prioritizes customer experience. Therefore objectives could be related to:

- Implementing customer relationship management systems (i.e. the company’s activity in social media).

- Establishing customer support service (i.e. call center responsible for customer concerns)

- Improving customer interaction (the process by which the company integrates customer feedback in R&D phase)

- Operational Excellence Strategy (cutting operational costs; achieving operational excellence).This could be implemented by a manufacturing company whose objectives focus on optimizing operational functioning. Specific objectives could draw inspiration from these themes:

- Decreasing operating costs and cycle time.

- Ensuring high standards of quality and delivery time.

- Optimizing supply chain.

- Product Leadership Strategy (creating new products and services; build the franchise).If it is heavily reliant on tech, the company can focus on this strategy. The objectives are mainly focused on:

-

- Choose specific objectives for the different perspectives based on the strategy determined initially (i.e. product leadership, customer intimacy, operational excellence). Note that objectives in different perspectives are interrelated. The completion of an objective in one perspective could help complete an objective in another perspective. Here, we will give examples of how to choose the objectives in the different perspectives based on the three mentioned generic strategies

- Financial perspective: As mentioned earlier, the typical financial goals for a company revolve around improving profits and revenue while cutting on costs. When looking at the three generic strategies, objectives can focus on:

- Developing new revenue streams via new products and services (product leadership strategy).

- Ameliorating profitability by improving customer value proposition (customer value strategy).

- Optimizing resources via cost reduction, scaling production or sharing resources between departments (operational excellence strategy).

- Customer perspective: In this perspective, goals are implemented to satisfy the customer by mapping what the customer wants from the company (and not the other way around). Therefore, based on the three generic strategies, objectives could include:

- Improving product quality (product leadership strategy).

- Optimizing customer experience (customer intimacy strategy).

- Improving pricing and timing (operational excellence strategy).

- Internal processes perspective: This perspective aims to improve the business’ inner systems in order to satisfy both customer needs and financial goals. Examples of such objectives include:

- Simplifying product initiation (product leadership strategy).

- Improving customer service and relationship management (customer intimacy strategy).

- Optimizing process flow by re-sequencing tasks (operational excellence strategy).

- Learning and growth perspective: Given the continuous evolution of the business world, there is a constant need for organizations to develop accordingly. Interestingly, this perspective adopts a different strategic framework when developing its objectives. There are three themes that this perspective focuses on, within which different objectives can be developed:

- Team capabilities theme (do the employees possess the skills required to achieve the internal perspective objectives?).

- Assess employee skills.

- Train employees.

- Strategy awareness and motivation theme (to ensure employees are motivated and understand the company strategy).

- Implement strategy awareness program.

- Improve leadership and motivation.

- Develop organizational culture.

- Information system capabilities theme (the information systems necessary to execute the company’s vision).

- Improve information system capabilities.

- Team capabilities theme (do the employees possess the skills required to achieve the internal perspective objectives?).

- Financial perspective: As mentioned earlier, the typical financial goals for a company revolve around improving profits and revenue while cutting on costs. When looking at the three generic strategies, objectives can focus on:

Below are examples of BSCs within the different generic strategies. For now, focus only on the main objectives within each perspective (the corresponding measures will be explained in the following sections of this manual). In the examples below, the companies have a main focus but it is key to observe that they show a proper execution of a balance between the different perspectives but also between different strategies. This is because it is crucial for a company to satisfy diverse needs in order to succeed in the industry. Moreover, these examples represent the concept of key measures which will be discussed in the following sections of this OER.

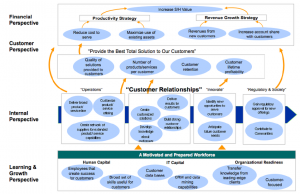

Customer intimacy strategy example:

Retrieved from: https://www.researchgate.net/figure/Strategy-map-template-for-customer-intimacy-or-complete-customer-solutions-Kaplan-and_fig5_255430269

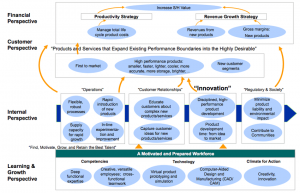

Product leadership strategy example:

Retrieved from: https://www.researchgate.net/figure/Strategy-map-template-for-product-leadership-Kaplan-and-Norton-2004-p-327_fig4_255430269

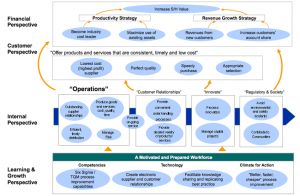

Operational excellence strategy example:

Retrieved from: https://www.researchgate.net/figure/Strategy-map-template-for-operational-excellence-or-best-total-cost-Kaplan-and-Norton_fig3_255430269

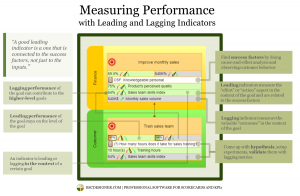

3. After we have specified the objectives required, we must complement them with appropriate indicators.Also known as Key Performance Indicators, KPIs are a metric that allow a company to set a standard of measurement. Consequently, this gives the ability to compare with past results or different companies, as well as plan ahead. These indicators will allow the company to measure progress based on specific criteria that best suit the strategic objectives. This is best explained by defining and giving examples of the types of indicators used.There are two types of indicators used:

Leading: Indicators that will positively influence/drive towards the desired outcome. This is considered to be a predictive measurement.

I.e. The percentage of people wearing hard hats on a building site is a leading safety indicator.

Lagging: this indicator is an output measurement and can only be used as a record to what has already happened.

I.e. the number of accidents on a building site is a lagging safety indicator.

Note: Lagging indicators can be considered reactive measurements while leading indicators can be considered proactive measurements.

Examples:

- Customer Service KPIs:

- Average speed of answer.

- Cost per inbound contact.

- Innovation KPIs:

- R&D budget.

- Revenue from new projects.

- Operational excellence KPIs:

- Time of product production.

- Cost per unit.

For a more detailed guide to KPIs: https://bscdesigner.com/kpis-guide.htm

Below is an infographic explaining the implementation of performance indicators (for more detailed information about this section, visit the origin of this infographic: https://bscdesigner.com/leading-vs-lagging.htm ).

4. Finally, we need to cascade internal objectives.Also known as “alignment”, cascading is applicable to all perspectives. This step involves translating the corporate-wide objectives (Tier 1) down to smaller subunits of the company such as departments (Tier 2) and teams/individuals (Tier 3). This allows the entire organization to maintain a clear understanding of the overarching strategy and vision. Moreover, this allows the corporate level to precisely pinpoint areas of strength and weakness and therefore allow improve the company’s productivity. As the management system is cascaded, objectives become more operational and strategic.

The process of cascading objectives basically revolves around finding the specific tasks required to complete the objective (objectives within objectives). This is exemplified in the example below: the company wishes to “provide customers with better product or service” (Tier 1), which requires building and presenting brand by the marketing team (Tier 2). Accordingly, the website team (Tier 3) within the marketing team will need to “provide engaging content” in order to “build and present brand”.

Retrieved from: https://bscdesigner.com/cascading.htm

Note how among the different tiers of the company, there is a constant alignment of strategy and objectives within different perspectives.

A case study with BSC in Toyota.

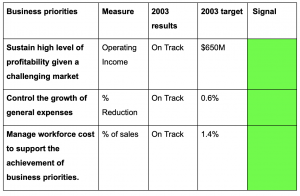

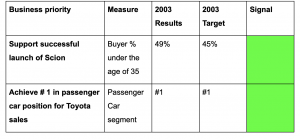

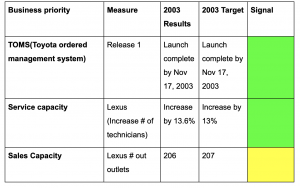

Toyota is one of the leading car companies in the world, originating from Japan but eventually manufacturing cars all over the world. In America, their mission statement is to be the most successful and respected car brand in America. To gain this success in 2003, Toyota management implemented a BSC. They began by creating a strategy to complement their mission statement like expand sales to youth buyers, expand shares of the SUV market and have the tops sales in passenger cars. Throughout this process, the executives maintained contact with their employees for feedback and updated them about their progress. This was done in order to align the company and ensure that the whole system understood the process and objectives of each goal. Through the employees’ feedback, Toyota was able to assess where they needed to improve on and create objectives to work on these weaknesses(Delta Publishing 2014).

After creating their overall strategies and listening to the feedback from their employees Toyota’s management started devising a way to incorporate these goals into a BSC. This meant having a balance between the four goals with some of the objectives overlapping with each other. For increasing financial goals they had tasks like control the growth of general expenses, manage workforce costs and also sustain a high level of profitability given a challenging market. While looking at the internal business process they had focused on expanding sales and service capability and focus on completing major technology process. Toyota also wanted to maintain its high level of customer loyalty, sustain a high level of dealership satisfaction and also improve customer and sales satisfaction. Lastly to improve their learning and growth they wanted a successful model launch, achieve #1 in passenger sales and maintain luxury SUV leadership(Delta Publishing 2014)..

Financial BSC

Learning and growth BSC

Internal Process BSC

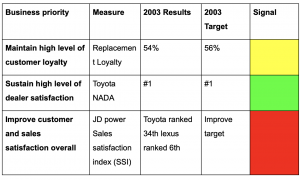

Customer Segment BSC

With Toyotas implementation of the BSC we can see their strategy succeed in many areas of their vision. The BSC shown above provides an excellent example of creating an understandable project for the employees and management to understand. With each objective to improve the company, they also included KPI’s to evaluate the progress of each of their goal. We can also see the crossing over of each of the four BSC perspectives, for example in learning and growth the successful launch of a new car will impact the financial goals of the company. The dashboard is also seen on the side of each BSC which shows the managerial team where the company is at with the targets. The BSC was able to benefit the employees, customers, and management in a different way. Employees saw more contribution from their work, managers saw increased profit and sales while improving customers loyalty. From Toyota, other companies can learn success and follow the BSC with a strategy of their own. It shows that financial success is not always the only measure of success and that other non-financial options can lead a company to be just as successful. The only thing Toyota could have improved on was a strategy map that would include the causal relationships between each goal(Delta Publishing 2014).

Conclusion:

The BSC is a strategic management tool helping to measure, monitor, and communicate strategic goals throughout the organization through an understandable way and get everybody on the same page working towards the same goals (Lawson et al. 2008). The BSC is a set of coherent performance measures providing executives with a comprehensive framework for an organization’s vision and strategy (Kaplan and Norton 1996a). Organizations are using the BSC to provide a quick look at whether or not they are achieving their goals and strategy. The BSC is considered as a mean of communication, informing, and learning system and should not be used as a controlling system (Kaplan and Norton 1996b). Top management of an organization can use the BSC to translate its strategy into performance measures that employees can easily understand. The BSC is organized into four perspectives: Learning and Growth perspective, Internal Process perspective, Customer perspective, and Financial perspective (Atkinson, Kaplan, Matsumura, and Young 2012).

References:

Atkinson, A.A., Kaplan, R.S., Matsumura, E.M., Young, S.M., (2012). Management Accounting, 6thEd. New Jersey, NJ: Pearson Education.

Atkinson, A., J. Waterhouse, and R. Wells (1997) A Stakeholder Approach to Strategic

Performance Measurement, Sloan Management Review (Spring).

Delta Publishing (2014)The Balanced scorecard: strategic based controls,

http://www.apexcpe.com/publications/371015.pdf

De Wet, Johannes & Jager, Phillip. (2007). An Appropriate Financial Perspective for a Balanced Scorecard.

Figge, F., Hahn, T., Schaltegger, S., & Wagner, M., (2002). The Sustainability Balanced Scorecard – Theory and Application of a Tool for Value-Based Sustainability Management. In Greening of Industry Network Conference, Gothenburg (p. 2).

Kaplan, R. S., & Norton, D. P. (2001). Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part I. Accounting Horizons, 15(1), 87-104.

Janota, R. M. G. (2008). The Balanced Scorecard in a pharmaceutical company.

Lawson, R., Hatch, T., & Desroches, D. (2008). Scorecard Best Practices: Design, Implementation, and Evaluation. Hoboken, NJ: John Wiley & Son.

Kaplan, R.S., & Norton, D.P., (1996a). Linking the Balanced Scorecard to Strategy.

California Management Review, 39(1).

Kaplan, R.S., & Norton, D.P., (1996b). The Balanced Scorecard: Translating Strategy

into Action. Harvard Business Press.

Kaplan, R. S. and D.P. Norton (1992) The Balanced Scorecard: Measures that Drive Performance,

Harvard Business Review, (January-February): 71-79.

Kaplan, R. S. and D.P. Norton (2003) Strategy Maps, Boston: HBS Press.

Kaplan, R. S. and D.P. Norton (2004b). Measuring the Strategic Readiness of Intangible Assets,

Harvard Business Review (February): 52-63

Kaplan, R. S. and D.P. Norton (2006a). Alignment: Using the Balanced Scorecard to Create

Corporate Synergies, Boston: HBS Press.

Kaplan, R. S. (2009). “Conceptual foundations of the balanced scorecard.” Handbooks of management accounting research 3: 1253-1269.

6 examples of balanced scorecards: https://www.clearpointstrategy.com/full-exhaustive-balanced-scorecard-example/

Demonstration of how to build BSC on website.

https://bscdesigner.com/try-bscdesigner

https://bscdesigner.com/internal-processes.htm