10 Cooking Loss Test

Some meats cannot be accurately portioned until they are cooked. This applies particularly to roasts, which shrink during cooking. The amount lost due to shrinkage can be minimized by incorporating the principles of low-temperature roasting, but some shrinkage is unavoidable.

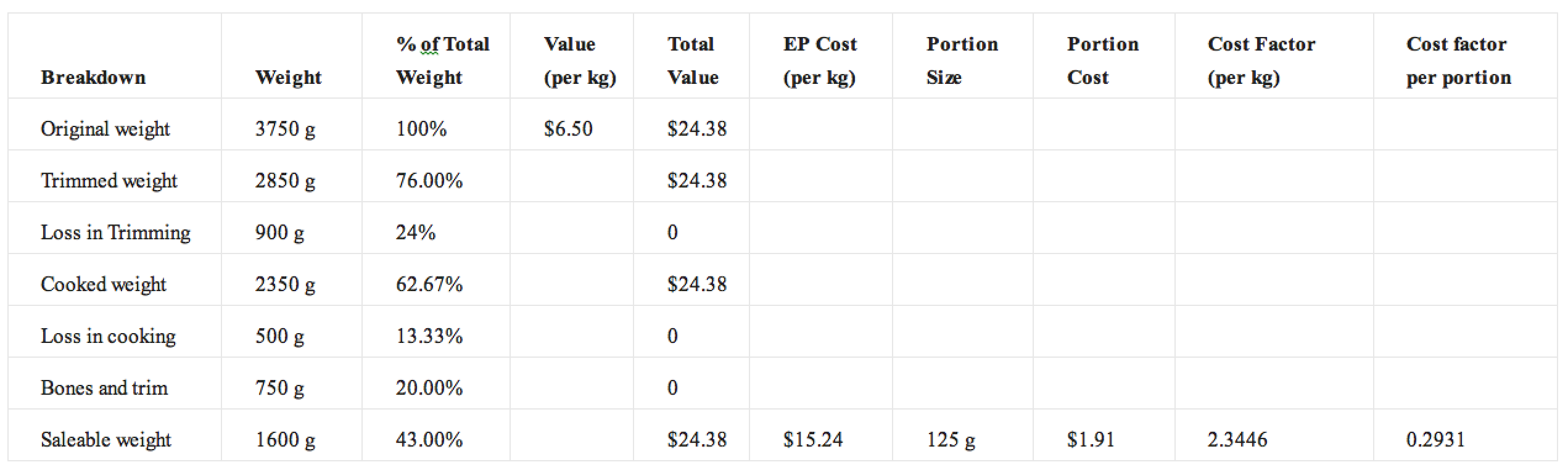

The cooking loss test serves the same function as the meat cutting yield test. Their similarities and differences will become evident in the discussion below. Figure 13 shows a sample cooking loss test form.

Cooking Loss Test

Item: Leg of Lamb

Portion: 125 g

Cost factor: 0.2931

Number cooked: One

Time: 2 hours and 30 minutes

Temperature: 175°C

Figure 13: Cooking loss test form

When using a cooking loss test form, note the following, referring to Figure 13:

- The form specifies the time and temperature of the roasting.

- The column headings are similar to the column headings on the meat cutting yield test form (Figure 12), as you are measuring similar things.

- The first line in Figure 13 lists the weight and wholesale cost of the roast (total value).

- The trimmed weight is the weight of the roast that is placed in the oven. Some fat and gristle has been trimmed off in the kitchen. In the example, about 900 g have been trimmed. Technically, if the trim has some value, it should be used to reduce the total value of the roast. However, for simplicity it is ignored in this example.

- After cooking for 2 hours and 30 minutes (the time stated on the test form), the roast is weighed and the cooked weight is entered on the form.

- The weight loss in cooking is determined by subtracting and the value entered on the form.

- The cooked roast is then deboned and trimmed. The weight of this waste is recorded.

- The weight of the remaining roast is determined. This is the amount of cooked roast you have available to sell and which can be divided into portions.

- Notice that the total value (that is, the cost) of the roast remains the same throughout the process. Only the weight of the roast changes.

- The percentage of total weight figures are calculated in the same way they were determined in Figure 12.

- The cost of usable kg is determined by dividing the saleable weight into the total value of the roast.

- Portion size is determined by restaurant managers, and the portion cost is calculated by multiplying the cost of usable kg and the portion size. This is the same procedure used to determine portion cost on the meat cutting yield test form.

- The cost factor per kg is the ratio of the cost of usable kg and the original value per kg.

Equation

cost factor per kg = cost of usable kg/value per kg

= $15.24/$6.50

= 2.3446

- The cost factor per portion is again found by multiplying the cost factor per kg by the portion size.

As with the meat cutting yield test, the most important entries on the cooking loss test sheet are the portion cost and the cost factor per kg as they can be used to directly determine the portion and kilogram costs if the wholesale cost unit price changes.

Yield percentages are the ratio to total weight values found for usable meat on the meat cutting yield test sheet and the saleable weight found on the cooking loss test. Once found, yield percentages (or yield factors as they are sometimes called) are used in quantity calculations.

The general relationship between quantity and yield percentage can be seen in the following equation:

quantity needed = (number of portions x portion size)/yield percentage

Equation

Find the quantity of pork loin needed to serve 50 people 250-g portions if the yield percentage is 52% as in Figure 12. The solution is:

quantity needed = (number of portions x portion size)/yield percentage

= (50 x 0.250 kg)/52%

= 12.5 kg/0.52

= 24.03 kg

You need just over 24 kg of untrimmed pork loin to serve 50 portions of 250 g each.

The yield formula can be restated in other ways. For example, if you needed to find how many 125 g portions of lamb can be served from 12 kg of uncooked lamb given a yield factor of 43%, you could use the following procedure:

Equation

number of portions = (quantity on hand x yield percentage)/portion size

= (12 kg x 0.43)/0.125 kg

= 5.16 kg/0.125

= 41.28

As with the inventory sheets, using a spreadsheet to help calculate the yields and factors is helpful. Some sample tools are provided in the Appendix.