Chapter 05. Internal Controls

05.04. Testing and Monitoring Controls

Key Questions

![]() Briefly reflect on the following before we begin:

Briefly reflect on the following before we begin:

- What methods are used to test the effectiveness of internal controls?

- How does continuous monitoring differ from traditional control testing methods, and what advantages does it offer?

- What role do internal auditors play in the testing and monitoring of controls?

- How should an organization respond to identified control deficiencies?

Testing and monitoring internal controls ensure their effectiveness and reliability within an organization. This section focuses on the methodologies and processes involved in evaluating the functionality of internal controls to identify any weaknesses or deficiencies.

Developing a comprehensive plan for testing internal controls is the initial step in this process. This plan outlines the objectives, scope, and methodologies for testing various control activities. Sampling, observation, and reperformance are commonly employed to assess control effectiveness across different business processes. Additionally, technology plays a crucial role in enhancing control testing and monitoring efforts. Automation tools, data analytics, and continuous monitoring systems enable organizations to streamline testing processes, identify anomalies more efficiently, and maintain real-time oversight of control activities.

Internal audit teams often play a significant role in testing, leveraging their expertise to assess control design and operational effectiveness. Continuous monitoring strategies, supported by automated tools and data analytics, facilitate ongoing control performance evaluation, enabling organizations to detect and address deviations or deficiencies promptly. When control deficiencies are identified, remediation processes are initiated to address the root causes and strengthen control frameworks. Ultimately, reporting on control effectiveness to management and the board provides transparency and accountability, enabling informed decision-making and driving improvements in control environments. Through diligent testing, monitoring, and remediation efforts, organizations can enhance the reliability and efficiency of their internal control systems, mitigating risks and safeguarding assets effectively.

Internal Audit in Action

Internal Audit in Action

Background

Rochdale Bank, a multinational banking institution, has faced several operational risks due to outdated and ineffective internal controls. Recognizing the need to bolster its control environment, the bank undertakes a significant initiative to revamp its control testing and monitoring practices to enhance operational resilience and compliance.

Challenge

The challenge for Rochdale Bank is to develop a comprehensive testing program that can accurately assess the effectiveness of internal controls across diverse operations. The bank must ensure that the program can identify weaknesses before they impact financial performance or compliance status.

Action Taken

The CAE leads the effort, implementing several key strategies:

- Developing a Risk-Based Testing Plan: The plan prioritizes testing activities based on the risk profile of different business units and processes, focusing on areas with the highest risk exposure.

- Adopting Advanced Testing Techniques: Rochdale Bank incorporates testing techniques, including sampling, observation, and reperformance, to evaluate control effectiveness. The bank also leverages data analytics to identify patterns indicative of control failures.

- Continuous Monitoring with Technology: Implementing continuous monitoring tools that utilize key risk indicators (KRIs) to flag potential control issues in real time, allowing for prompt corrective action.

- Strengthening the Feedback Loop: Establishing mechanisms for reporting testing results to management and the board, ensuring they are informed of control effectiveness and areas needing improvement.

- Training and Awareness: Conduct regular training sessions for employees involved in control testing to ensure they are up to date with the latest methodologies and technologies.

Outcome

Rochdale Bank’s revamped control testing and monitoring program significantly improves the effectiveness of internal controls. Early detection of control weaknesses enables timely remediation, reducing operational and compliance risks. Advanced testing techniques and continuous monitoring tools provide deeper insights into control performance, enhancing the bank’s overall risk management capabilities.

Reflection

This scenario highlights the importance of a systematic and risk-based approach to testing and monitoring internal controls. Rochdale Bank’s experience demonstrates how leveraging technology and focusing on high-risk areas can improve the efficiency and effectiveness of control testing programs, thereby strengthening the organization’s control environment and risk management practices.

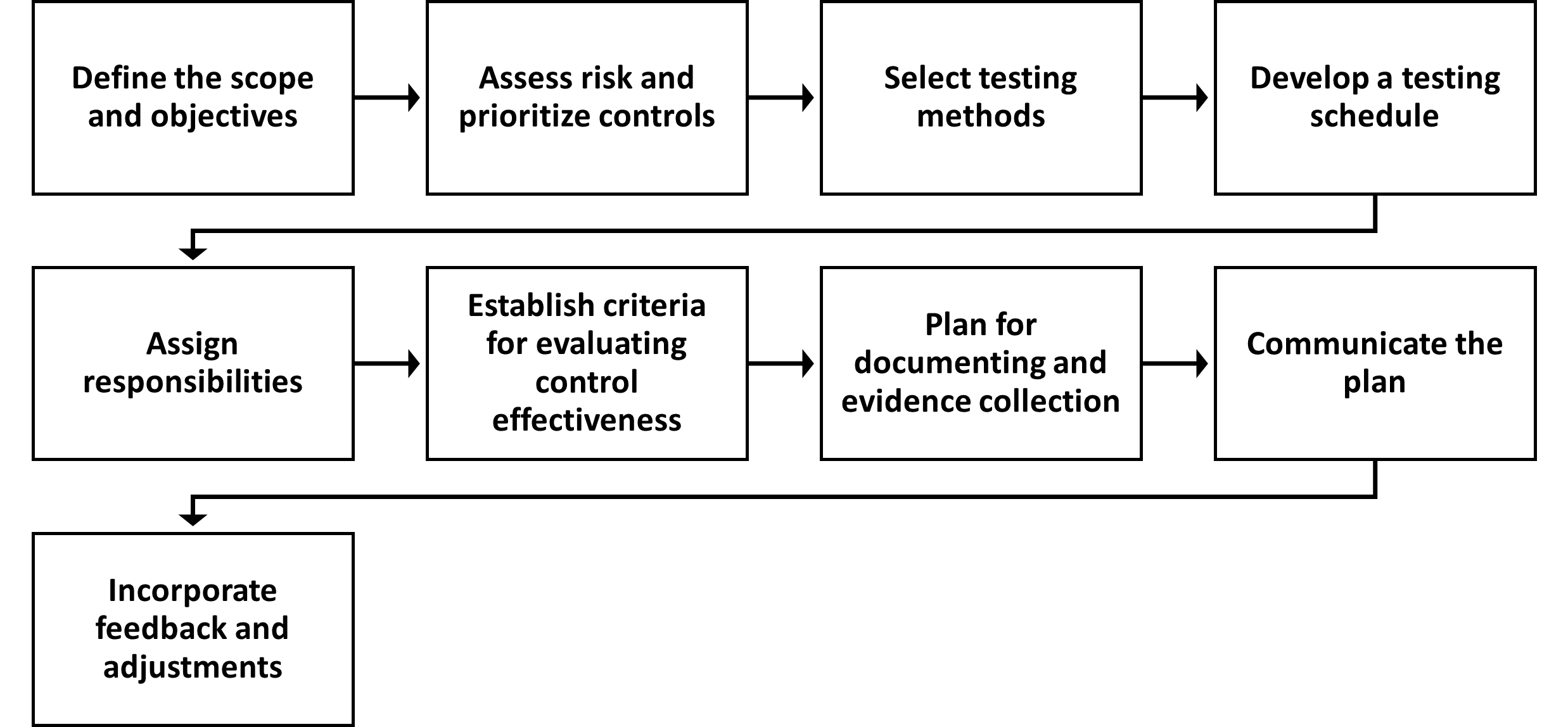

Developing a Plan for Testing Internal Controls

Developing a plan for testing internal controls ensures that an organization’s control environment is adequate and functioning as intended. This process involves establishing objectives, methodologies, timelines, and responsibilities to assess the adequacy and effectiveness of internal controls. A well-designed testing plan enables an organization to identify control weaknesses, ensure compliance with laws and regulations, and mitigate risks.

- Define the Scope and Objectives

- Start by defining the scope of the testing plan, including identification of the specific controls to be tested, the areas or processes they pertain to, and the testing objectives.

- Objectives may include assessing control effectiveness, compliance with policies and procedures, and identification of areas for improvement.

- Assess Risk and Prioritize Controls

- Conduct a risk assessment to identify high-risk areas within the organization.

- Controls related to high-risk areas should be prioritized for testing.

- This approach ensures that testing efforts focus on controls that are critical to the organization’s risk management strategy.

- Select Testing Methods

- Choose appropriate testing methods based on the nature of the controls and the testing objectives.

- Standard techniques include sampling, observation, inquiry, inspection of documents, and reperformance of control activities.

- The selection of methods should consider the reliability of evidence needed and the efficiency of the testing process.

- Develop a Testing Schedule

- Create a detailed schedule that outlines when and how each control will be tested.

- The schedule should consider the availability of resources, the timing of business cycles, and any external factors that may impact testing, such as regulatory reporting deadlines.

- Assign Responsibilities

- Assign responsibilities for each aspect of the testing plan by identifying the individuals or teams responsible for conducting tests, analyzing results, and reporting findings.

- Ensure that personnel with the appropriate expertise and independence are assigned to test controls.

- Establish Criteria for Evaluating Control Effectiveness

- Define the criteria that will be used to evaluate the effectiveness of controls including criteria for assessing the adequacy of control design, the consistency of control application, and the effectiveness of control operations in mitigating risks.

- Plan for Documentation and Evidence Collection

- Determine how evidence of control testing will be documented and retained by specifying the types of evidence to be collected, how documentation will be organized, and how long evidence will be retained.

- Proper documentation supports the findings of the testing process.

- Communicate the Plan

- Communicate the testing plan to relevant stakeholders, including management, process owners, and the internal audit function.

- Ensure that all parties know the testing objectives, methodologies, and responsibilities and can provide support.

- Incorporate Feedback and Adjustments

- Be prepared to incorporate feedback and adjust the testing plan as necessary.

- Based on preliminary findings or changes in the organization’s risk environment, changes to the testing plan may involve revisions to the scope, testing methods, or the plan schedule.

Exhibit 5.2 shows the steps required to develop a plan for testing internal controls.

Techniques for Testing Controls: Sampling, Observation, and Reperformance

Techniques for testing controls are vital for assessing the effectiveness of an organization’s internal control system. Through these techniques, auditors and internal control specialists can gather evidence about how healthy controls are designed and operated. Three primary techniques used in the testing process include sampling, observation, and reperformance. Each method offers unique insights and helps identify potential control deficiencies.

Sampling

Sampling involves selecting and testing a subset of transactions from a larger population. This technique is used when testing every transaction is either impractical or unnecessary. Sampling can be either statistical or non-statistical. In statistical sampling, the sample size and selection process are determined mathematically to allow for conclusions about the entire population with a known confidence level. In non-statistical sampling, judgment is used to select the sample. Sampling helps auditors assess control effectiveness and estimate the rate of control failures across the population, providing a basis for evaluating the overall reliability of controls.

Observation

Observation involves directly watching a process or control being performed. This technique helps understand how controls are applied in practice and verifies that they operate as described in policies and procedures. Through observation, auditors can assess whether employees follow prescribed processes, such as security protocols at a data centre or cash handling procedures at a retail outlet. However, it’s important to note that observation is time-bound; it provides evidence of control operation at a specific moment in time and may not capture variations in how controls are applied over time.

Reperformance

Reperformance is a technique where the auditor independently executes control procedures to verify their effectiveness. For example, an auditor might reperform the reconciliation process for bank accounts or test the accuracy of inventory counting procedures. Reperformance provides direct evidence of a control’s effectiveness by allowing the auditor to confirm firsthand that the control operates as designed and achieves the desired outcome. This technique is beneficial for complex controls or where there is a high risk of misstatement or fraud.

Synergies between the Various Testing Techniques

Each of these testing techniques has its strengths and limitations. Sampling provides a broad overview of control effectiveness across transactions but may not capture all instances of control failures. Observation offers real-time evidence of control application but may be influenced by the observer effect, where individuals modify their behaviour because they are being watched. Reperformance provides conclusive proof of control operation but can be resource intensive. A combination of these techniques is often used to comprehensively assess an organization’s internal controls. By carefully selecting the most appropriate testing techniques based on the control objectives, risks, and available resources, organizations can effectively evaluate the effectiveness of their internal control systems, identify areas for improvement, and take necessary corrective actions to strengthen their control environment.

Using Technology to Aid in Control Testing and Monitoring

Using technology to aid in control testing and monitoring represents a significant advancement in how organizations assess and ensure the effectiveness of their internal controls. Technology provides tools and systems that can automate the testing and monitoring processes, enhance accuracy, increase efficiency, and provide real-time insights into control performance.

For starters, automated control testing tools can perform repetitive tasks without human intervention, significantly reducing the time and resources required for control testing. These tools can automatically execute tests on a wide range of controls, from access controls in IT systems to transaction controls in financial systems, providing evidence of control operation and effectiveness. Automation also facilitates frequent testing, enabling organizations to promptly identify and address control issues. Continuous monitoring systems also leverage technology to assess real-time control performance and risk indicators. These systems can detect deviations from expected control operations or predefined thresholds, alerting management to potential control failures or emerging risks. Continuous monitoring technologies, such as data analytics and business intelligence platforms, analyze vast amounts of operational and transactional data, offering insights to inform risk management and control enhancement strategies.

Data analytics and business intelligence tools can process large datasets to identify patterns, trends, and anomalies that may indicate control weaknesses or failures. By applying advanced analytics techniques, such as predictive analytics or machine learning, organizations can gain deeper insights into their control environment, enhancing their ability to manage risks proactively. Technology facilitates the creation of dashboards and automated reports that provide management and the board with clear, concise, and real-time visibility into the status of controls and risk management activities. These tools can aggregate data from various sources, presenting it in an easily digestible format that supports informed decision-making and strategic planning. Technological solutions, such as identity and access management systems, encryption, and intrusion detection systems, are essential for testing and monitoring IT-related controls. These technologies help protect against unauthorized access and cyber threats, ensuring the integrity and security of the organization’s information assets.

While technology offers significant benefits for control testing and monitoring, organizations must consider challenges such as the cost of implementing technology solutions, the need for specialized skills to operate advanced systems, and ways to ensure the security and privacy of the data used in testing and monitoring processes. Additionally, reliance on technology should not detract from the need for human judgment and expertise in interpreting data and making informed decisions. Thus, leveraging technology in control testing and monitoring can significantly enhance an organization’s ability to assess the effectiveness of its internal controls, identify and address issues promptly, and support a robust risk management framework. As technology evolves, organizations that effectively integrate these tools into their control environments will be better positioned to manage risks and achieve their strategic objectives.

The Role of Internal Audit in the Testing Process

The role of internal auditing in the testing process of internal controls is pivotal, acting as an independent and objective assurance and consulting function designed to add value and improve an organization’s operations. Through a systematic, disciplined approach, the internal audit function helps an organization accomplish its objectives by evaluating and improving the effectiveness of risk management, control, and governance processes.

At the onset, an internal audit provides an independent assessment of the organization’s internal control system, offering unbiased insights into the effectiveness of controls. This independence is vital for ensuring that the testing process is objective and that findings and recommendations are impartial, providing management and the board with confidence in the control testing results.

Internal auditing adopts a risk-based approach to control testing, focusing resources on areas of highest risk to the organization. By aligning the testing process with the organization’s risk profile, the internal audit function ensures that control testing is strategic, targeted, and aligned with the organization’s overall risk management strategy. This approach helps identify and address potential control weaknesses that could significantly impact the organization’s ability to achieve its objectives.

Internal auditing utilizes testing techniques, including sampling, observation, and reperformance, to evaluate internal control design and operating effectiveness. This comprehensive approach allows internal audits to gather sufficient evidence to assess whether controls function as intended and identify areas where controls may be lacking or ineffective.

A critical aspect of the role of an internal auditor is to identify control deficiencies during the testing process and communicate these findings to management and the board. An internal audit provides detailed reports outlining identified weaknesses, the potential risks associated with these weaknesses, and recommendations for improving controls. This communication is essential for ensuring that management is aware of control issues and can promptly address them. After recommendations have been made to address control deficiencies, internal audits verify that corrective actions have been implemented effectively. This follow-up process ensures that control improvements are carried out as planned and effectively mitigates identified risks.

Beyond testing and identifying deficiencies, internal audits also serve as a valuable resource for management by advising on best practices in internal control and suggesting improvements to enhance the control environment. This advisory role can help organizations strengthen internal controls, reduce risks, and improve operational efficiency. The internal audit function also contributes to the continuous improvement of the internal control system by regularly reviewing and testing controls, providing feedback on the effectiveness of control improvements, and staying informed about changes in the business environment, risks, and regulatory requirements that may necessitate adjustments to controls.

Continuous Monitoring: Strategies and Tools

Continuous monitoring represents an integral component of an organization’s internal control system, enabling real-time or near-real-time assessment of control performance and effectiveness. Through constant monitoring, organizations can detect and respond to risks and changes in control effectiveness as they occur rather than relying on periodic reviews. This proactive approach enhances the organization’s ability to manage and mitigate risks effectively.

Continuous monitoring, supported by effective strategies and advanced technological tools, allows organizations to maintain a robust control environment responsive to changing risks and operational demands. By implementing continuous monitoring, organizations can enhance their risk management capabilities, improve operational efficiency, and assure management and the board that critical controls are functioning effectively.

Strategies for Continuous Monitoring

The following are some of the most commonly used strategies for continuous monitoring:

Integration with Business Processes

Continuous monitoring should seamlessly integrate into the organization’s business processes. This integration ensures that monitoring activities are part of daily operations, making it easier to identify and address issues promptly.

Risk-Based Approach

Organizations should prioritize continuous monitoring activities based on risk assessments. High-risk areas, critical processes, and essential controls should be monitored more frequently and rigorously to ensure they function effectively and mitigate risks as intended.

Automated Alerts and Triggers

Establishing automated alerts and triggers based on predefined criteria or thresholds can facilitate early detection of control failures or deviations from expected performance. These alerts enable prompt investigation and remediation of issues.

Regular Review and Adjustment

Continuous monitoring processes should be reviewed and adjusted regularly to reflect changes in the organization’s risk profile, business environment, and operational processes. This adaptability ensures that monitoring activities remain relevant and effective over time.

Tools for Continuous Monitoring

The following are some of the most commonly used tools for continuous monitoring:

Data Analytics and Business Intelligence Software

These tools can analyze large volumes of transactional data to identify patterns, trends, and anomalies that may indicate control issues or emerging risks. Advanced analytics can provide insights into operational efficiency and control effectiveness.

Dashboards and Reporting Tools

Dashboards provide real-time visibility into key performance indicators (KPIs), control metrics, and risk indicators. Customizable reporting tools allow organizations to generate reports that support decision-making and risk management.

Automated Control Testing Tools

Automated testing tools can perform routine control tests without human intervention, providing continuous assurance of control effectiveness. These tools are handy for testing IT controls, such as access controls and data integrity checks.

Security Information and Event Management (SIEM) Systems

SIEM systems are used to continuously monitor IT security controls. They collect and analyze security-related data from various sources, detecting potential security incidents and enabling rapid response.

Compliance Management Software

This software helps organizations monitor compliance with regulatory requirements and internal policies. It can track compliance activities, manage documentation, and alert management to potential compliance issues.

Responding to Control Deficiencies: Remediation Processes

Responding to control deficiencies involves a systematic remediation process to address weaknesses or failures in an organization’s internal control system. When control deficiencies are identified, organizations must act promptly to mitigate risks, prevent recurrence, and ensure the effectiveness of their control environment.

The remediation process includes the following steps:

Assessment

The first step is to thoroughly assess the identified control deficiencies to understand their nature, causes, and potential impact on the organization. This type of internal control assessment helps categorize deficiencies based on their severity, such as whether they represent a material weakness, significant deficiency, or a minor control gap. Understanding the scope and implications of deficiencies is critical for prioritizing remediation efforts.

Planning

Based on the assessment, a detailed remediation plan should be developed to address the identified deficiencies. The plan should outline specific corrective actions, assign responsibility for implementing these actions to appropriate personnel or departments and establish deadlines for completion. Remediation actions may include revising existing controls, implementing new controls, enhancing training programs, or modifying operational processes.

Implementation

With the remediation plan in place, the next step is to implement the corrective actions. This may involve modifying policies and procedures, upgrading technology systems, enhancing security measures, or providing additional employee training. Effective communication and change management practices are essential during this phase to ensure that all affected personnel understand the changes and their roles in the remediation process.

Monitoring

After corrective actions are implemented, it’s necessary to monitor the effectiveness of these efforts and conduct testing to verify that the deficiencies have been successfully addressed. This may involve repeating the initial testing procedures used to identify the shortcomings or employing additional testing techniques as appropriate. Ongoing monitoring helps ensure that remediated controls are operating as intended and that no new issues have arisen due to the changes made.

The Importance of the Remediation Process

Thorough documentation should be maintained throughout the process to record the findings, actions taken, and results of remediation efforts. This documentation is critical for internal records, audit trails, and compliance. It’s also important to report on the status of remediation efforts, outcomes, and any remaining risks to management and the board. This reporting ensures accountability and assures that control deficiencies are addressed. The remediation process and outcomes should be reviewed to identify lessons learned and opportunities for continuous improvement in the internal control system. This review can inform future risk assessments, control designs, and testing strategies, enhancing the organization’s control environment.

Responding to control deficiencies through a structured remediation process is essential for maintaining the integrity and effectiveness of an organization’s internal control system. By systematically addressing deficiencies, organizations can strengthen their controls, mitigate risks, and enhance their governance and risk management capabilities.

Reporting on Control Effectiveness to Management and the Board

Reporting control effectiveness to management and the board is a critical final step in the internal control process. It ensures that those responsible for oversight and strategic decision-making are well-informed about the strength of the control environment, existing deficiencies, and the actions taken to address them. Effective reporting facilitates transparency, accountability, and informed governance.

Control effectiveness reports are essential to an organization’s internal control and governance processes. These reports ensure that management and the board are well-informed and engaged in overseeing and strengthening the control environment. Effective reporting supports strategic decision-making, risk management, and regulatory compliance, ultimately contributing to the organization’s success and resilience.

Here’s an overview of how reporting on control effectiveness should be approached:

- Comprehensive Coverage

- Reports should cover all critical aspects of the control environment, including the design and operation of controls, control testing results, identified deficiencies, and the status of remediation efforts.

- Comprehensive coverage ensures that management and the board have a holistic view of the organization’s internal control system.

- Clear and Concise Presentation

- Plain language, visual aids like charts and graphs, and executive summaries can help distill complex information into digestible and actionable insights.

- Risk-based Prioritization

- Reports should highlight issues based on risk implications by focusing on the most significant deficiencies that could impact the organization’s ability to achieve its objectives.

- Prioritization helps management and the board focus on areas of highest concern.

- Action Plans and Responsibilities

- For each identified control deficiency, the report should include a detailed action plan for remediation, including specific steps to be taken, individuals or departments responsible for remediation, and expected timelines for resolution.

- This clarity supports accountability and ensures that corrective actions are promptly and effectively implemented.

- Progress Tracking

- Reporting should not be a one-time activity but part of an ongoing process to track the progress of remediation efforts and reassess control effectiveness.

- Regular updates to management and the board on the status of action plans reinforce the organization’s commitment to maintaining a robust internal control system.

- Compliance and Regulatory Considerations

- Reports should address compliance with relevant laws, regulations, and standards where applicable, ensuring the organization meets its external obligations.

- This is especially essential for organizations in highly regulated industries.

- Strategic Implications

- Beyond detailing operational control issues, reports should also discuss the strategic implications of the control environment including how control deficiencies might impact the organization’s strategic objectives and how enhancing controls can support strategic goals.

- Engagement and Dialogue

- Reports serve as a basis for dialogue between management, the board, and other stakeholders, such as internal and external auditors.

- This engagement fosters a collaborative approach to risk management and control improvement.

- Confidentiality and Security

- Sensitive information contained in the reports should be handled with appropriate confidentiality and security to protect the organization’s interests.

Internal Audit in Action

Background

Cortes Canada, a leading logistics and supply chain management company, has experienced rapid growth. An internal audit reveals challenges in maintaining effective oversight of internal controls. To address these challenges, Cortes Canada embarks on a transformation of its control monitoring processes.

Challenge

Cortes Canada’s primary challenge is implementing a monitoring system that can keep pace with its dynamic business environment, ensuring controls remain effective as the company evolves.

Action Taken

The Director of Risk Management spearheads the transformation, focusing on:

- Implementing Dashboards and Scorecards: Cortes Canada develops custom dashboards and scorecards that give management a real-time overview of control effectiveness and areas of concern.

- Regular Reviews and Adjustments: Instituting a schedule for regular, comprehensive reviews of the control environment and individual control activities to assess their continued relevance and effectiveness.

- Leveraging Automation for Real-Time Monitoring: Adopting automation and machine learning technologies to monitor transactions and operations continuously for signs of control failures or deviations from expected patterns.

- Engaging Frontline Employees: Encouraging frontline employees to participate in the monitoring process by reporting anomalies and control failures, supported by a user-friendly reporting platform.

- Feedback Mechanism for Continuous Improvement: Establishing a robust feedback mechanism that collects insights from control testing and monitoring activities to inform continuous improvement in the control framework.

Outcome

The transformation of control monitoring processes at Cortes Canada results in a more agile and responsive control environment. Real-time dashboards and automated monitoring enable quick identification and remediation of control issues. The active engagement of employees at all levels fosters a culture of accountability and continuous improvement. The enhanced monitoring processes significantly reduce operational risks and improve compliance, supporting Cortes Canada’s growth and operational efficiency.

Reflection

Cortes Canada’s scenario illustrates the transformative impact of advanced monitoring technologies and employee engagement on the effectiveness of internal controls. By adopting a proactive and technology-driven approach to control monitoring, organizations can ensure their control systems remain robust and responsive in the face of rapid growth and changing business landscapes, safeguarding against risks and enhancing operational performance.

Key Takeaways

Key Takeaways

Let’s recap the concepts discussed in this section by reviewing these key takeaways:

- A robust plan for testing internal controls outlines the scope, objectives, methodologies, and timelines for assessing control systems. It’s about identifying what needs testing, when, how, and by whom, ensuring a comprehensive evaluation of the organization’s defences against potential threats and inefficiencies.

- Testing controls involving techniques such as sampling, observation, and reperformance. Sampling allows for evaluating control effectiveness across various transactions, observation provides real-time insights into the application of controls, and reperformance verifies the operational integrity of controls.

- Internal audit is the cornerstone of the testing process, offering an independent and objective assessment of the internal controls landscape. Through a risk-based approach, the internal audit function identifies, tests, and reports on the effectiveness of controls, ensuring that the organization’s risk management, governance, and control processes are operating effectively.

- Identifying control deficiencies is only part of the equation; effectively responding to them through structured remediation processes is vital. This involves diagnosing the root cause, developing corrective action plans, assigning responsibilities, and setting timelines for resolution.

- Transparent and comprehensive reporting on control effectiveness to management and the board is essential for informed oversight and decision-making. It includes providing details of control performance, highlighting deficiencies, outlining remediation efforts, and discussing the strategic implications of the control environment.

Knowledge Check

Knowledge Check

Review Questions

Review Questions

- What is the primary goal of developing a plan for testing internal controls within an organization?

- Describe one technique used for testing internal controls and explain its significance.

- How does technology aid in the control testing and monitoring process?

- What role does Internal Audit play in the testing process of internal controls?

- Why is continuous monitoring necessary in the context of internal controls?

Essay Questions

- Discuss the importance of developing a comprehensive plan for testing internal controls and outline the steps an organization should take to create such a plan. How does this plan contribute to the overall effectiveness of the internal control system?

- Explain the significance of continuous monitoring in the context of internal controls and describe the strategies and tools that can be employed to implement an effective continuous monitoring system. How does continuous monitoring complement traditional testing methods?

Mini Case Study

Oke Manufacturing Co., a medium-sized enterprise, has experienced rapid growth over the past two years. With expansion into new markets and the introduction of several new product lines, the complexity of Oke’s operations has significantly increased. Consequently, the company’s CEO is concerned about the existing internal control system’s ability to effectively manage the heightened risk environment.

To address these concerns, the CFO has proposed an initiative to enhance the company’s internal control system, focusing on implementing more robust testing and monitoring processes. The plan includes developing a comprehensive testing plan for critical controls, employing new technology for continuous monitoring, and strengthening the role of internal auditing in the testing process.

As part of the initiative, Oke Manufacturing Co. has decided to test its inventory management controls due to significant variances noted between recorded inventory levels and physical counts. The company plans to use a combination of sampling, observation, and reperformance techniques for testing, integrate continuous monitoring tools to track inventory transactions in real time and rely on internal audits to provide an independent control environment assessment.

Required: Given the scenario above, how should Oke Manufacturing Co. enhance its internal control system to address the increased complexity and risk? Specifically, discuss how the company should develop its testing plan, the role of technology in monitoring inventory controls, and the contribution of the internal audit function in ensuring the initiative’s effectiveness.

The process of evaluating the effectiveness of an organization's internal controls to ensure they are mitigating risks and achieving objectives.

A deficiency, or a combination of deficiencies, in internal control, resulting in a reasonable possibility that a material misstatement of the financial statements will not be prevented or detected on a timely basis.

A deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness but important enough to merit attention.

A weakness in the design or operation of a control that does not allow management to prevent or detect misstatements on a timely basis.

Ongoing evaluations to ensure that control activities are functioning as intended and deficiencies are addressed in a timely manner.